Interest Types

- 29 Mar 2023

- 6 Minutes To Read

- Print

- DarkLight

- PDF

Interest Types

- Updated On 29 Mar 2023

- 6 Minutes To Read

- Print

- DarkLight

- PDF

Article Summary

Share feedback

Thanks for sharing your feedback!

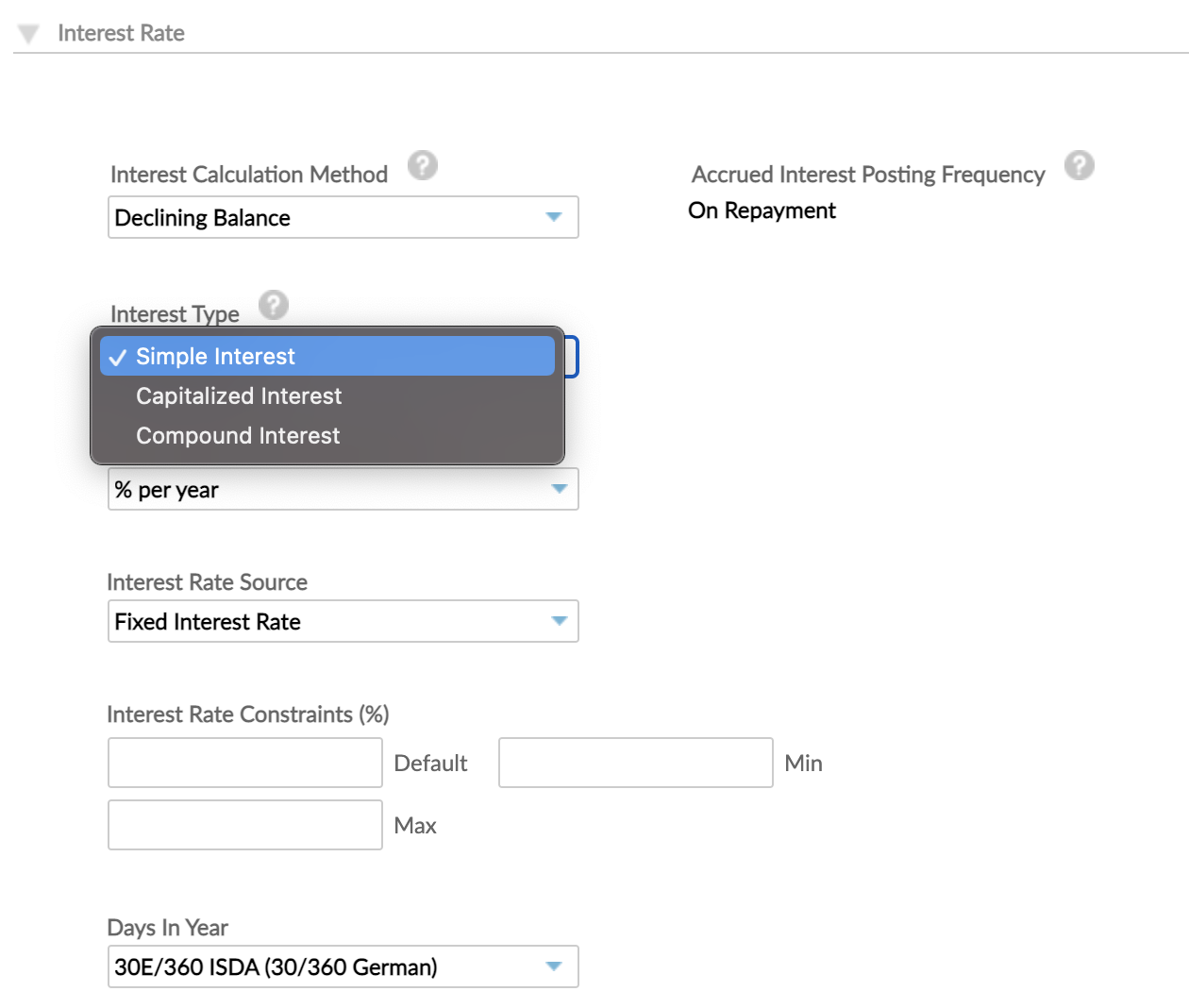

Set up the interest type of a loan product

When setting up new loan products, in the Interest Rate section of the form, choose between the following Interest Types to define the interest frequency and formula you want to apply to your loan products:

- Simple interest

- Capitalized interest

- Compound interest

Simple interest

Simple Interest is the default interest type for all loan product types using Flat, Declining Balance or Declining Balance (Equal Installments) interest calculation methods.

Formulas

Simple interest type is based on the linear formula and it is determined by multiplying the daily interest rate by the principal, and then by the number of days that elapse between payments and divide by the number of days in the year.

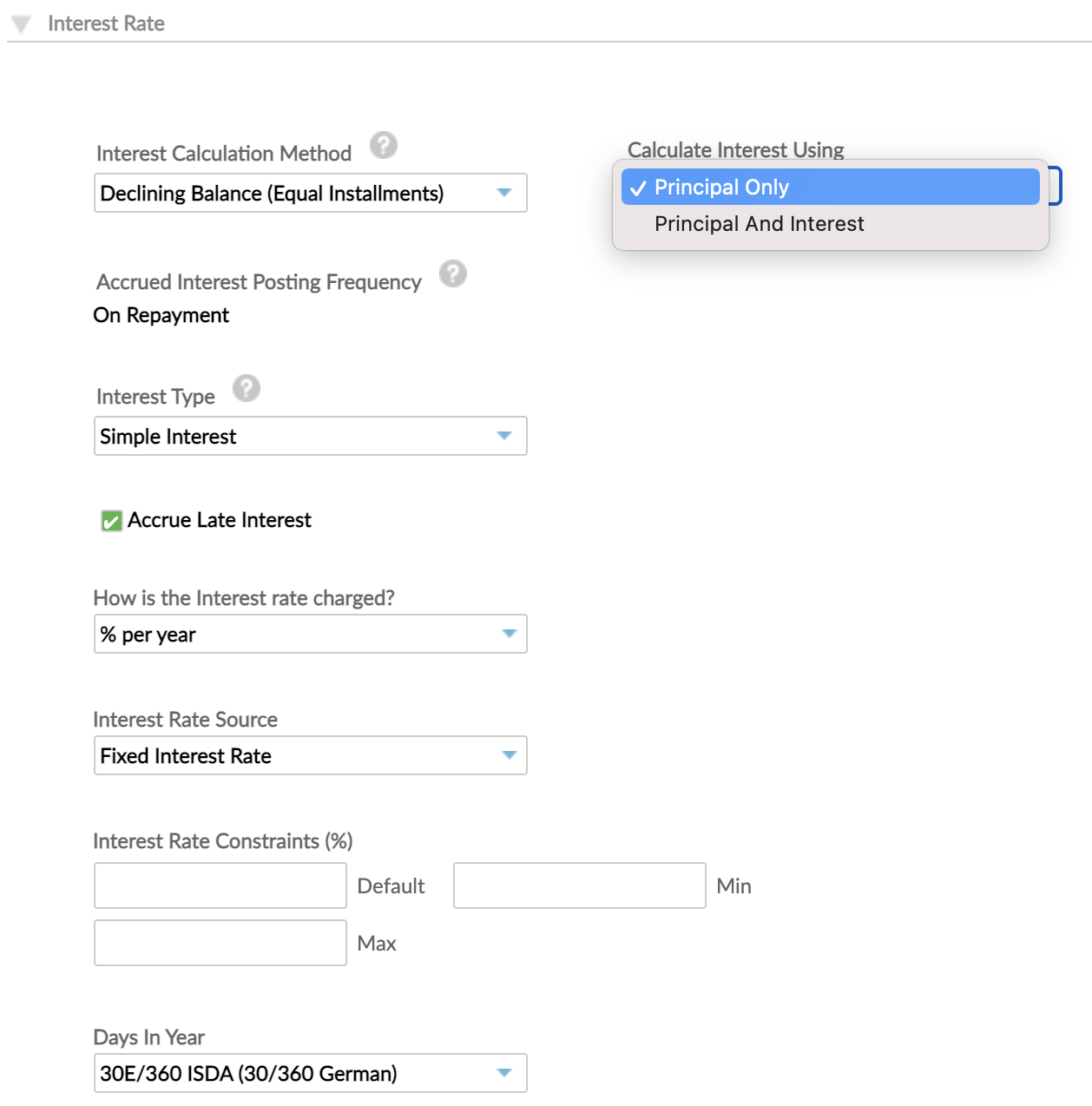

where Base Balance can be calculated using two methods:

- Principal Only

- Principal and Interest

By default, the base balance used in the interest formula calculation is Principal Only, which represents the Outstanding Principal Balance from the loan account, so we will have the following formula:

Principal and Interest is available only for dynamic term loans with the Declining Balance (Equal Installments) method, and calculates the interest by multiplying the daily interest rate by the principal and unpaid interest and then by the number of days that elapse between payments and divide by the number of days in the year.

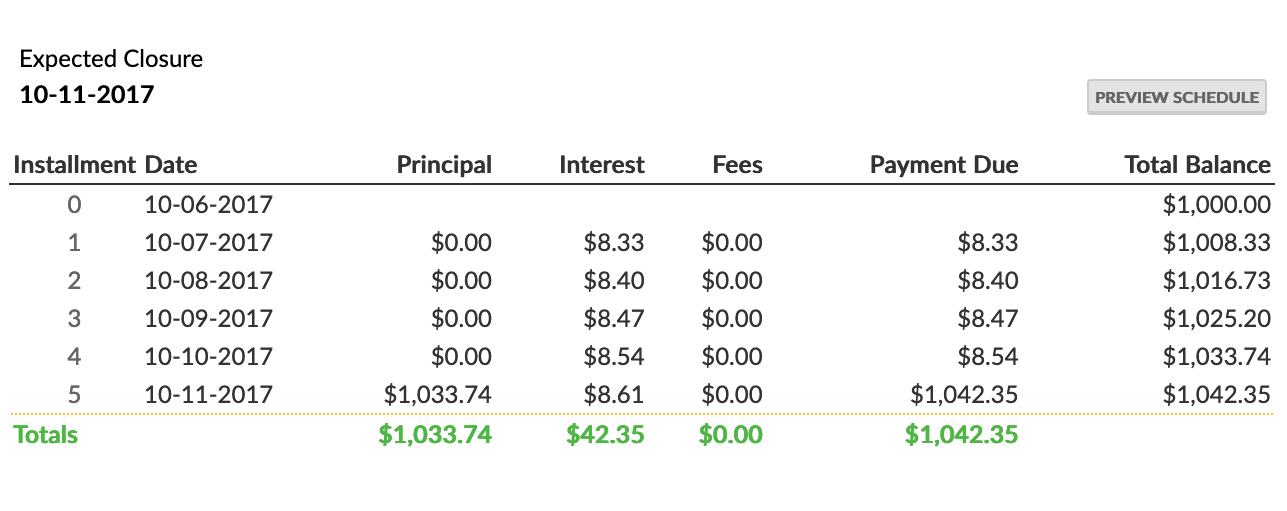

Example

The following is an example of Principal and Interest calculation. Consider a loan with the following terms:

- Loan amount: USD1000

- Interest Rate (IR%): 10% per year

- No of installments: 5

- Monthly Repayments

- Disbursement date: January 1, 2020

- Total Due (PMT): USD205.03

- Days in Year method: 30/360

First installment February 1, 2020

Interest Amount = (Outstanding Principal Balance + Interest Balance) * IR% * NoOfDays/360 = (USD1000+USD0) * 10% * 30 / 360 = USD8.33

If we apply the interest, Interest Balance will be USD8.33.

Second installment March 1, 2020

Interest Amount = (Outstanding Principal Balance + Interest Balance) * IR% * NoOfDays/360 = (USD1000+USD8.33) * 10% * 30 / 360 = USD8.40

If we apply the interest, the Interest Balance will be:

Interest Balance = Interest applied on the first installment + Interest applied on the second installment = USD8.33 + USD8.40 = USD16.73

After it is applied, the interest is updated in the schedule with the new calculation based on Principal and Interest.

Please Note

If the repayments are paid on time, the interest balance will always be 0, and this method will act exactly like the Principal Only interest calculation method.

Accounting

When simple interest is applied, it will be considered as an income from the accounting point of view.

The following journal entries for the accrual accounting methodology are logged at interest application:

- Debit: Interest Receivable

- Credit: Interest Income

When the interest will be paid, the following journal entries will be entered:

- Debit: Transaction Source

- Credit: Interest Receivable

Capitalized interest

The Capitalized Interest type means that, when the interest is applied, it is capitalized (applied) into the principal balance. This method is available for Dynamic Term loans with both the Declining Balance and the Declining Balance (Equal Installments) calculation methods.

For Declining Balance with Capitalized Interest, the first (total-1) installments are by default principal grace installments. So, after applying interest in each due date, all the principal amount (which contain the interest amount as well) will be allocated on the last installment.

For the Declining Balance (Equal Installments) calculation method with the capitalized interest, the installments will have both principal and interest expected.

Formula

Capitalized interest is calculated as simple interest type with Principal Only base:

Example

Consider a dynamic declining balance loan with the following terms:

- Loan amount: USD1000

- Interest Rate: 10% per year

- No of installments: 5

- Monthly Repayments

- Disbursement date: June 10, 2022

- Days in Year method: 360

The schedule generated with capitalized interest type based on the above loan terms is:

See below the calculations implied in this case:

Interest Expected = Outstanding Principal Balance * Annual Interest Rate % * NoOfDays / DaysInYear = USD1000 * 10% * 30/360 = USD8.33

Payment Due = USD8.33

Accounting

From the accounting perspective, capitalized interest and simple interest are different. When it is applied, the interest is capitalized on the principal balance and the following journal entries are logged in accounting:

- Debit: Portfolio Control

- Credit: Interest Income

When the interest will be paid, only the principal amount will be paid in the end, having the following journal entries:

- Debit: Transaction Source

- Credit: Portfolio Control

Compound interest

Compound interest is the interest calculated on the original principal and all the accumulated previously paid interests. An easier way to think of compound interest is that is it “interest on interest,” where the amount of the interest payment is based on changes in each period, rather than being fixed at the original principal amount.

Frequency

The compounding frequency determines how many times the interest is paid and it influences the interest rate itself. In Mambu, the interest is compounded daily, meaning that each interest accrued will be calculated based on the principal balance and the accrued interest from the previous day.

Formulas

Unlike the simple interest, which is based on a linear formula (see above), the compound interest is based on the following exponential formula:

Compound interest calculation formulas in Mambu:

| Convert annual interest rate to a smaller period | Formula |

|---|---|

| From IR% per year to Annual Interest Rate | |

| From IR% per year to Monthly Interest Rate | |

| From IR% per per year to 4 weeks Interest Rate | |

| From IR% per year to Weekly Interest Rate | |

| From IR% per year to Daily Interest Rate |

Compound Interest has a direct implication in the Periodic Payment (PMT) formula as well, being calculated as:

where the periodic rate is calculated based on the formulas from the above table. For more information about the PMT function, go to How to Calculate Loan Payments with Excel PMT Function.

Please Note

Compound interest type is available for all loan product setups, except for:

- Fixed Term loans with Repayments Interest Calculation as using repayment periodicity

- Revolving Credit

Example

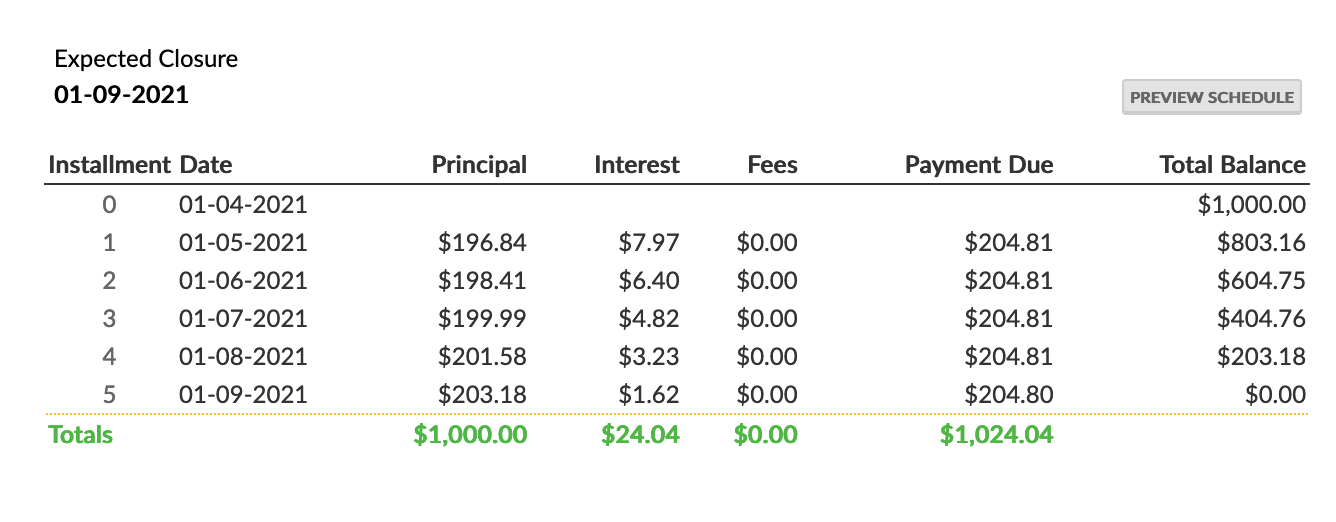

Example of loan account with compound interest rate:

Loan Amount: USD1000

Interest Rate: 10% per year

No of installments: 5

Days in Year method: 30E/360

Monthly Repayments

The schedule generated with compound interest type based on the above loan terms is:

See below the calculations implied in this case:

Monthly Interest Rate = (1+ Annual Interest Rate%)^(1/12)-1 = 0.80%

Payment Due = PMT(Monthly Interest Rate, no of installments, -Loan amount) = USD204.81

Interest Expected = Outstanding Principal Balance * ((1+Annual Interest Rate%)^(30/360)-1) = USD7.97

Principal Expected = Payment Due - Interest Expected = USD196.84

For more detailed calculations, see this file:

Accounting

From the accounting point of view, the compound interest is similar with the simple interest. When Compound interest is applied, it will be considered as an income from the accounting point of view. The following journal entries for accrual accounting methodology are logged at interest application:

- Debit: Interest Receivable

- Credit: Interest Income

When the interest will be paid, the following journal entries will be entered:

- Debit: Transaction Source

- Credit: Interest Receivable

Was this article helpful?